Job Costing for Small Contractors: A Simple System That Actually Works

Most small contractors don’t lose money because they lack work. They lose money because they don’t have a clear system for understanding what their jobs actually cost. On the surface, everything can look fine. The project is moving forward, invoices are being sent, and cash is coming in. But when the job wraps up, the margin is far smaller than expected, or worse, completely gone.

This gap between expectation and reality is almost always caused by poor job costing.

If you cannot clearly see your costs during a job, you are not controlling your profit—you are reacting to it.

Job costing, at its core, is the process of tracking every dollar that goes into a specific project. The challenge is not the concept. The challenge is consistency, especially for small contractors juggling multiple responsibilities.

A proper job costing system allows you to answer key questions at any moment:

- How much have we spent so far?

- What remains in the budget?

- Are we over or under?

- What is our projected profit right now?

If you cannot answer these quickly, your system is not working.

The first step is setting a complete job budget before work begins. Many contractors underestimate this step, focusing only on labor and materials. That creates blind spots immediately.

A complete budget should include:

- Labor (including burden)

- Materials (including waste and delivery)

- Subcontractors

- Equipment

- Overhead

If your budget is incomplete, every decision you make from it will be flawed.

Once the budget is defined, the real work begins—tracking costs in real time. This is where most contractors fail. They update numbers at the end of the week or after the job is complete, which turns job costing into a historical record instead of a decision-making tool.

Costs must be tracked as they happen:

- Labor recorded daily

- Materials logged at purchase

- Unexpected costs added immediately

Small expenses are easy to ignore, but over time they compound into major margin loss.

Profit doesn’t disappear all at once—it leaks out through untracked details.

As the project progresses, comparing budget versus actual costs becomes critical. This is the moment where job costing provides real value.

For example:

- Labor exceeds budget halfway through

- Materials trend higher than expected

At this stage, you still have options:

- Adjust labor allocation

- Reduce future spending

- Improve efficiency

If you wait until the end, there is nothing left to fix.

Another major blind spot for small contractors is overhead. Expenses like insurance, admin time, vehicles, and tools are often ignored because they are not tied directly to a single job.

Over time, this leads to:

- Underpricing jobs

- Overestimating profit

- Tight cash flow

Ignoring overhead does not improve profit—it hides the truth.

Spreadsheets are often the first attempt at solving job costing, and they can work at a small scale. But as complexity increases, they begin to fail.

Common issues include:

- Manual updates

- Outdated data

- Multiple versions of the truth

- No real-time visibility

Spreadsheets track information, but they do not manage execution.

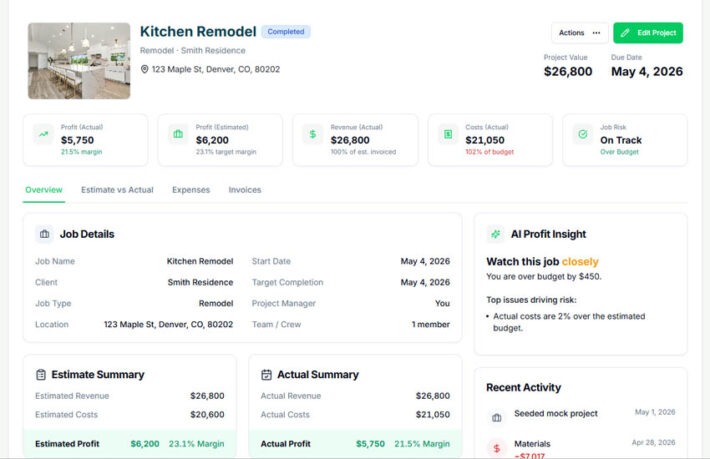

A connected system changes how job costing works. With WorkBalance, budgets, expenses, and projects are tied together, allowing you to see your financial position as the job progresses.

This enables you to:

- Monitor profit in real time

- Catch issues early

- Adjust before margin disappears

The shift from tracking to managing is what creates control.

Every completed job should also be reviewed. This is where improvement happens.

After each project, evaluate:

- Where costs exceeded expectations

- What was underestimated

- What should change next time

Over time, this builds a system that gets stronger with every job.

Job costing does not need to be complex to be effective. It needs to be consistent, visible, and integrated into how you actually run your business.

If you want better margins, you need better visibility—everything else follows from that.