How to Estimate Jobs (Step-by-Step Guide for Small Businesses)

Most small businesses don’t lose money because they lack work.

They lose money because they estimate jobs incorrectly.

At first, estimating feels simple. You look at the job, think about how long it will take, add a number that feels right, and send it to the client. Sometimes you win the job. Sometimes you don’t.

But what matters isn’t whether you win the job.

It’s whether the job actually makes money.

And that’s where most businesses struggle.

Because once the work begins, reality sets in:

- Jobs take longer than expected

- Costs increase

- Scope expands

- Small expenses get missed

By the time the project is finished, the margin you thought you had is gone.

That’s the problem.

Estimating isn’t just about pricing—it’s about building a system that protects your profit.

Why Most Estimates Fail

The reason most estimates fail is simple:

They are based on assumptions, not data

You might estimate:

- 10 hours of labor

- $200 in materials

- Straightforward execution

But in reality:

- It takes 14 hours

- Materials cost $300

- Extra work is required

That gap is where profit disappears.

If your estimate isn’t based on real numbers, it’s just a guess.

What a Good Estimate Actually Does

A good estimate doesn’t just give a price.

It answers three critical questions:

- What will this job cost?

- How long will it take?

- Will it be profitable?

If your estimate can’t answer those, it’s incomplete.

Step 1: Define the Scope Clearly

Every estimate starts with scope.

This is where most mistakes begin.

You need to understand:

- What exactly is included

- What is not included

- What could change

Ask:

- What tasks are required?

- Are there unknowns?

- Are there potential add-ons?

The more detailed your scope, the more accurate your estimate.

Unclear scope leads to unexpected work—and lost profit.

Step 2: Break the Job Into Tasks

Once you define the scope, break the job down into smaller pieces.

Instead of estimating one big number, estimate:

- Individual tasks

- Time per task

- Resources needed

This creates clarity.

For example:

- Prep work → 2 hours

- Main work → 6 hours

- Cleanup → 1 hour

Now you’re not guessing—you’re building.

Step 3: Calculate Labor Costs

Labor is usually your largest cost.

Start with:

- Hourly rate

- Number of workers

- Time required

Example:

- 2 workers

- 8 hours

- $30/hour

Labor = $480

But don’t stop there.

You must include:

- Payroll taxes

- Overtime risk

- Inefficiency buffer

Underestimating labor is the #1 reason jobs lose money.

Step 4: Add Materials and Direct Costs

Next, include all direct costs:

- Materials

- Supplies

- Subcontractors

- Equipment

Be realistic.

Add a buffer for:

- Price increases

- Waste

- Unexpected needs

Small misses here can quickly erode profit.

Step 5: Include Overhead

This is where most businesses fail.

Overhead includes:

- Insurance

- Software

- Marketing

- Admin time

These aren’t tied to one job—but they still cost you money.

If you don’t include overhead, you’re underpricing every job.

A simple approach:

Add 10–30% to cover overhead

Step 6: Add Profit Margin

Now comes the most important part:

Profit

After all costs, you must add margin.

Typical ranges:

- 10% (low margin)

- 20–30% (healthy business)

Example:

- Total cost = $1,000

- Add 25% → Price = $1,250

This ensures you’re not just covering costs—you’re growing.

Step 7: Choose Your Pricing Model

Now that you know your cost, choose how to present it.

Common models:

Fixed Price

Best for repeatable work

Hourly

Best for unpredictable jobs

Per Unit (sq ft, room, etc.)

Best for fast quoting

The model doesn’t matter as much as the accuracy behind it.

Step 8: Build a Professional Estimate

Your estimate should include:

- Scope of work

- Pricing breakdown

- Timeline

- Terms

This does two things:

- Builds trust

- Prevents misunderstandings

A clear estimate wins better clients.

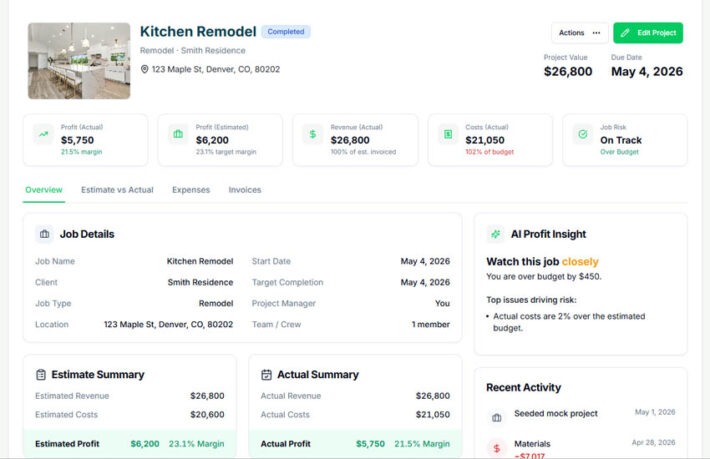

Step 9: Track Actual Results

This is the step most businesses skip.

After the job is complete, compare:

- Estimated cost vs actual cost

- Estimated time vs actual time

- Expected profit vs real profit

This is how your estimates improve.

Without feedback, your estimates never get better.

The Biggest Problem: Estimating Without a System

Most businesses estimate in isolation.

They:

- Use spreadsheets

- Write notes

- Rely on memory

But nothing connects:

- Projects

- Tasks

- Costs

- Profit

This is why estimates stay inaccurate.

How WorkBalance Fixes Estimating

WorkBalance connects everything.

Instead of guessing, you can:

- Build projects from estimates

- Track tasks and time

- Capture real expenses

- Compare estimate vs actual

- See profit in real time

This turns estimating into a system—not a one-time guess.

Every job makes your next estimate better.

What Happens When You Estimate Correctly

When your estimates are accurate:

- You stop underpricing

- You avoid bad jobs

- You protect margins

- You build predictable revenue

You move from guessing…

To controlling your business.

Final Thought

Estimating isn’t about getting the number right once.

It’s about building a system that gets better over time.

Most businesses estimate → execute → move on.

The best businesses:

Estimate → track → improve → repeat

Take Control of Your Estimates

WorkBalance helps you:

- Build accurate job estimates

- Track real costs and time

- Compare estimate vs actual

- See profit before the job is done

Because estimating isn’t about winning jobs—it’s about making money on them.