How to Price a Job for Profit (Without Guessing or Undercutting Yourself)

Pricing a job feels deceptively simple.

You estimate the work, add a margin, and present a number. The client either accepts it or pushes back. Over time, you adjust based on experience, competition, or instinct.

But here’s the problem—most pricing decisions are not based on real data. They’re based on what feels right.

And “feels right” is where profit quietly disappears.

Because pricing is not just about winning the job. It’s about ensuring that when the job is complete, it actually contributed to your business in a meaningful way.

That requires more than estimation. It requires control.

The Pricing Illusion Most Businesses Operate Under

There’s a common assumption that if a job brings in revenue, it must be profitable. That assumption is reinforced when cash flow looks healthy and work keeps coming in.

But revenue is not profit.

A job priced at $10,000 can feel like a win. But if the true cost of delivering that job is $9,200, the margin is far thinner than it appears. And if small overruns occur—as they almost always do—that margin can disappear entirely.

The illusion is not obvious because the numbers are rarely connected in real time. Costs are tracked separately, time is estimated loosely, and profit is calculated after the fact.

By then, it’s too late to change anything.

Pricing without visibility is just guessing with confidence.

What “Pricing for Profit” Actually Means

Pricing for profit is not about choosing a higher number. It’s about understanding the relationship between cost, time, and outcome before the work begins.

At a basic level, pricing needs to account for:

- Direct costs (materials, subcontractors, etc.)

- Labor (time required to complete the job)

- Overhead (business expenses that support the work)

- Desired profit margin

But the real challenge is not identifying these components—it’s estimating them accurately and consistently.

That’s where most businesses struggle.

The Hidden Variable: Time

Time is the most underestimated factor in pricing.

It’s easy to calculate material costs or subcontractor fees because those are visible and defined. Time, however, is fluid. It expands and contracts based on complexity, communication, and unexpected issues.

A job estimated at 20 hours can easily become 28 hours without anything going “wrong.” A few extra revisions, a delay in communication, or a small complication can add hours without being noticed in the moment.

Those extra hours don’t show up on an invoice—but they directly impact your margin.

If you don’t price your time accurately, you’re discounting your work without realizing it.

The Difference Between Estimated Profit and Actual Profit

Most pricing decisions are based on estimated profit. You calculate what you expect the job to cost, apply a margin, and move forward.

But actual profit is determined by what really happens during execution.

The gap between estimated and actual profit is where problems occur.

If your estimates are consistently lower than reality, your pricing will always be off. You may win jobs, but your margins will shrink over time. If your estimates are too high, you risk losing work to competitors.

Closing this gap requires feedback—real data from completed jobs that informs future pricing decisions.

Pricing Without Feedback Is a Loop

Many businesses operate in a loop:

- Estimate a job

- Price it

- Complete the work

- Move on to the next job

What’s missing is a clear comparison between what was expected and what actually happened.

Without that comparison, there is no learning. The same assumptions are used repeatedly, and the same mistakes are repeated.

Pricing becomes a cycle of approximation instead of a process of improvement.

The Role of Margin in Pricing

Margin is often misunderstood as a fixed percentage that can be applied across all jobs. In reality, margin is a reflection of risk.

Jobs with higher uncertainty—complex scope, tight timelines, or variable requirements—require higher margins to account for potential overruns. Simpler, more predictable jobs can operate with tighter margins.

Applying the same margin to every job ignores these differences.

Pricing for profit requires adjusting your margin based on the characteristics of the work.

Margin is not a constant—it’s a decision based on risk.

Why Undercutting Happens

Many businesses underprice their work without realizing it. This often happens in competitive situations where the focus shifts from profitability to winning the job.

When pricing is based on what competitors might charge, rather than what the job actually costs, margins become secondary.

The problem is that competitors may have different cost structures, different efficiencies, or different goals. Matching their price does not guarantee matching their profit.

Winning a job at the wrong price is not a win.

A Better Approach: Pricing as a System

Instead of treating pricing as a one-time decision, it should be treated as a system that evolves over time.

That system includes:

- Tracking actual costs and time for each job

- Comparing estimates to real outcomes

- Adjusting future pricing based on that data

- Monitoring profitability as work progresses

When pricing is part of a system, it becomes more accurate with each job.

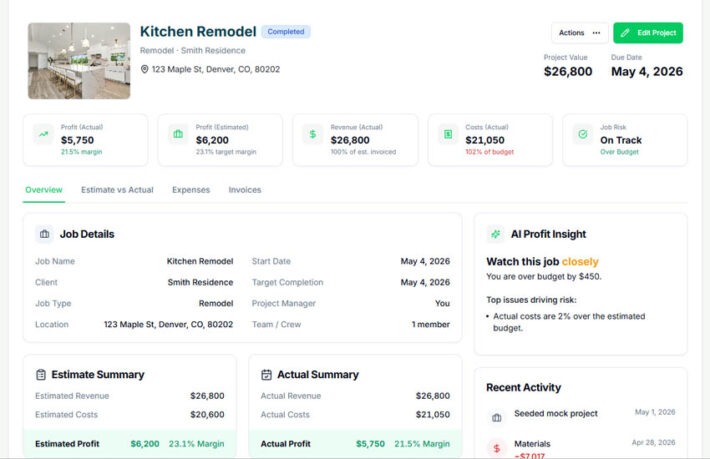

How Real-Time Visibility Changes Pricing

One of the most powerful ways to improve pricing is to see how a job is performing while it is happening.

If costs begin to exceed expectations, you can identify the issue early. If time is being spent inefficiently, you can adjust your approach. These insights feed directly into future pricing decisions.

Real-time visibility turns pricing into a feedback loop instead of a guess.

How WorkBalance Helps You Price for Profit

WorkBalance connects the pieces that most businesses struggle to align.

Instead of estimating in isolation, you can use real data from past projects to inform your pricing. As work progresses, costs and time are tracked automatically and tied to the job.

This allows you to:

- See how your estimates compare to reality

- Understand your true cost per job

- Adjust pricing based on actual performance

- Monitor profit as the job unfolds

Over time, this creates a system where pricing becomes more precise, margins become more consistent, and profitability becomes predictable.

You stop guessing your price and start knowing your numbers.

The Long-Term Impact of Better Pricing

When pricing is aligned with reality, everything improves.

You spend less time correcting mistakes. You avoid jobs that are not worth the effort. You build a portfolio of work that consistently delivers strong margins.

Perhaps most importantly, you gain confidence.

Pricing conversations become easier because you understand your value. You’re not negotiating from uncertainty—you’re operating from clarity.

Final Thought

Pricing is not just about setting a number. It’s about understanding the relationship between your work and its financial outcome.

When that relationship is clear, pricing becomes a tool for growth. When it’s unclear, pricing becomes a source of risk.

The difference is visibility.

Profit is not created when you invoice—it’s created when you price correctly.

Take Control of Your Pricing

WorkBalance helps you:

- Track real costs and time per job

- Compare estimates vs actual results

- Improve pricing accuracy over time

- See profit as work happens

Because the right price is the one that protects your profit.